The disruptions to residential education this spring have been substantial, and now the higher education sector in the United States is looking ahead to a highly uncertain fall term. Higher education has a very different revenue structure in the United States than in many other countries, and many of its components are at risk. Capital markets are concerned, and at least some individual institutions face an existential threat, but much remains unknown about the extent of the downturn facing the sector. College and university leaders recognize the unpredictable nature of the immediate future, yet circumstances demand that they make decisions and take actions. For people and organizations that provide services to universities, the uncertainty that has emerged in the sector during the past two months is vexing. Not every decision they make will be the right one, many organizations will suffer, and some will even collapse — and yet there may be strategic opportunity as well.

Budget Components

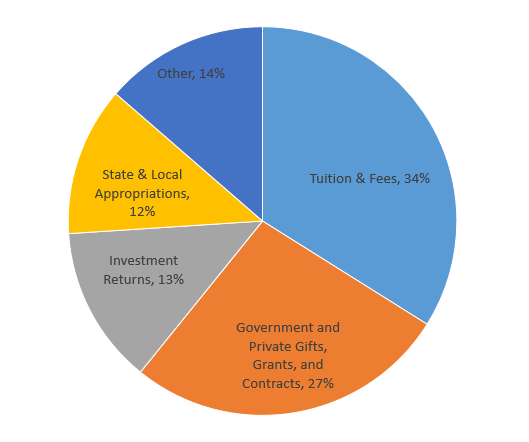

There are four main components to higher education institution revenues in the United States. The relative dependence on each of these four sources varies by institution type, as discussed below. This piece focuses on the not-for-profit and public institutions that grant a bachelor’s degree or higher. All revenue calculations are derived from the US Department of Education’s IPEDS database for the 2017-2018 data year, restricted to 4-year public and not-for-profit institutions in eight Carnegie Classifications for bachelor’s, master’s, and doctoral institutions. All percentages are based on aggregate revenues (and so will differ from other analyses that are weighted by institutions or enrollments). On this basis, doctoral institutions dominate US higher education, accounting for 80% of revenue among public institutions and 75% among private institutions.

Tuition and Fees. Tuition, as well as ancillary student fees such as room and board, constitute the plurality of revenues at higher education institutions in the United States that grant a bachelor’s degree or higher. Tuition, in this case meaning what is actually paid to the university rather than the sticker price, is of foremost importance for public institutions (where it accounts for 31% of revenue) as it is for private institutions (where it accounts for 38%). And although there is wide variance by individual institutions, tuition is of foremost importance across institutional types, from liberal arts colleges to research universities.

Many institutions refunded at least a portion of room and board in the spring term that was disrupted. Where a summer session is being contemplated, enrollments reportedly are lagging behind patterns in previous years.

Looking ahead, tuition revenues are at risk for three reasons.

- Loss of International Enrollments: Higher education is one of the most important export sectors in the United States. International students are a major profit center for many higher education institutions, because they typically pay sticker price. While international enrollments were already declining, in light of present circumstances, it is difficult to imagine many new international students choosing to begin their education in the United States this fall. Roughly one-third of international enrollments were from China, which may be at particular risk given geopolitical tensions. To the extent that international enrollments can be replaced with domestic enrollments, net tuition per student is likely to decline. Out of state students typically pay higher tuition than in-state students at public institutions. So, similar dynamics of lost revenue may be expected if fewer US students enroll in public institutions out of state.

- Increased Financial Need: Given the economic downturn resulting from the stay at home orders, including resulting unemployment, many families will find it more difficult to pay tuition. Some who otherwise would have attended four year institutions will likely choose to attend two year institutions instead (a prospect that has become more appealing for academically minded students in the states that have established pathways for completing a two-year associates degree and then transferring to a public institution to complete the bachelor’s degree). As a result, enrollments in the four year sector could decline along with resulting tuition. And, many students who enroll at four year institutions will require greater financial aid (often in the form of tuition discounts) in order to attend. If institutions meet this need rather than requiring students and families to take out loans, this will reduce net tuition per student.

- The Residential Model at Risk: Finally, the issue that has received the most attention is the uncertainty about the fall term. At a minimum, we can probably expect some modifications to instructional scheduling and delivery models. If it is not possible for an institution to provide residential education, it may be difficult to sustain enrollments at established tuition levels, particularly at residential institutions where the holistic on-campus experience has been used to justify higher tuition rates. Even if the fall term can occur through normal residential instruction, many currently graduating high school seniors are contemplating a delay in their college start or other alternatives. Some higher education leaders have predicted that a failure to return to some kind of residential model for education this fall could be catastrophic for the sector as a whole and certainly for some especially tuition-dependent private institutions.

The exact magnitude of the reduction in tuition revenues will probably vary widely. Those with the strongest national and international brands and highest selectivity will be in a relatively strong position in some ways. But many of these have also made substantial commitments to need blind admissions and meeting the full financial need of all students, which commitments will become more expensive if they are maintained. Those less selective public institutions whose business model has relied on international enrollments will face real challenges. Private institutions with more localized brand awareness and lower selectivity, and for which tuition constitutes an especially high share of revenues, had already faced substantial headwinds and now are likely at greatest risk.

Today, many institutions are finding that it is nearly impossible to forecast the exact financial circumstances they will face. Instead, they are waiting until later in May or June to see how matriculations (and deposits) and deferrals are shaping up for the upcoming academic year as well as indications of their ability to return to some kind of residential model of instruction.

Direct Public Support. Most of US public higher education receives direct government support principally from the states. There are exceptions, such as the military academies. In the aggregate, US higher education secures 12% of its revenue from the direct state support, with public institutions securing 22% of their revenues in this way, though this varies greatly between states and among institutions in the same state.

State budgets are funded by a variety of different tax regimes (income, sales, and property taxes, for example), and all of them are under tremendous pressure in any economic downturn. Some state funding cuts have already been announced. In some states, higher education may be a particular target for cuts, while in other states the sector may be comparatively protected. In the aggregate, however, it is fair to anticipate that the longer and deeper the downturn, the more likely that the states will reduce their funding for public higher education. In addition to operating support, states generally fund a significant share of capital spending in their public universities, which might be expected to decline substantially as a result unless included in stimulus spending.

Endowment and Gifts. Private gifts and investments represent an especially important source of revenue for private institutions. Both rely on wealth creation and maintenance and therefore ultimately to some degree on the health of the financial markets.

Many higher education institutions have built up an endowment. These are funds that are invested in perpetuity to provide spendable proceeds, which are typically restricted to certain purposes, such as a named professorship or a financial aid fund. Some portion of the funds that are invested as endowments are not actually restricted even though they are generally treated as such. Investment income accounts for 25% of the revenue of private institutions and 4% of the revenue of public institutions. Investment strategy differs by endowment size and various other factors. While the public markets were down substantially in March, they recovered some of their losses in April, though it is hard to be bullish about the medium term. Alternative investments are a major part of some endowments, and asset categories such as private equity and natural resources are hardly immune from an impact. Spending from these investments is cyclical with asset performance, although a spending rule will typically smooth the impact of losses (or gains) so that its impact is felt in the institution’s budget gradually over a period of several years. So, although losses in the current fiscal year will typically not yield required spending cuts until the 2021/22 fiscal year, many institutions will ask departments to smooth even further than the rule, in anticipation of the following year’s cuts. As for unrestricted investments, these can, at the institution’s discretion, be used as a “rainy day fund,” but there is typically tremendous resistance to spending down this capital asset.

In addition, many higher education institutions raise gifts for capital and annual spending (in addition to gifts to be invested in the endowment). These generally will decline in magnitude during an economic downturn. In that case, capital spending (especially on the physical plant) will be reduced substantially as a result, especially at private institutions.

Funded Research. In the US, the federal government is the most important source of funding for university research, larger than all other sources combined. Government grants and contracts account for 16% of revenues to higher education (and reach 19% at the universities with very high research activity). In one sense, there is no reason to anticipate reductions in federal research funding, since federal spending on research has only increased in recent months. At the same time, the current administration has sought a number of substantial cuts in research funding, most continuously to the arts and humanities, but also to scientific grant overheads, the latter of which, if ever implemented, would be financially devastating to research universities. Other research funders, such as private foundations that are funded from their own endowments, may reduce their spending in response to any long-term market downturn.

Other Revenue Sources. The above items constitute the most important sources of educational and general revenues for academic institutions. There are however several other revenue sources, each of which now has its own challenges. For one, a number of major research universities operate a hospital and healthcare system. For them, cancelled clinical care and elective procedures as a result of the pandemic will represent a major reduction in clinical revenues. And many institutions have a wide array of ancillary revenue streams, including facilities rentals, summer camps, arts performances, and parking, all of which have faced substantial disruption.

Implications

The picture that is emerging for the US higher education sector is fairly grim. Most institutions anticipate substantial losses in revenue from tuition, although its magnitude remains highly uncertain for the time being. Many institutions will also expect to see reductions in revenues from endowment spending, spendable gifts, and state support. And, while the federal government has provided some emergency aid to the higher education sector, it only scratches the surface.

For the time being, many institutions are taking a cautionary approach. Many are eliminating discretionary spending and are implementing hiring freezes and beginning furloughs or layoffs. In the absence of any real forecasts for the fall, however, many institutions are undertaking scenario planning to model a number of possibilities without yet re-forecasting their budgets for the upcoming fiscal year, pending more information.

Even with this uncertainty, it is not impossible to begin to predict the implications for academic library budgets. It is clear that most academic libraries will see a substantial budget reduction in the upcoming academic year. In a series of roundtables with academic library directors in recent year, my colleague Kimberly Lutz and I heard about some of the strategic and operating directions and dilemmas that academic library leaders today are facing. We heard many estimates of budget reductions in the 10% to 20% range, beyond the hiring freezes and other personnel moves already underway.

For publishers, cutbacks in the academic library channel cannot be good news. Questions abound. Has the library channel for print books disappeared only temporarily or now permanently? How much added pressure on subscriptions will journal publishers now see, given that the Big Deal model was already facing pushback? Will publishing intensive institutions continue to be willing to pay more for transformative agreements? Will they continue to seek pure publish agreements? Will Subscribe to Open models be sustainable in an environment of cutbacks?

The news may not all be negative however. While the academic library is the most important revenue channel for the scholarly publishing community, federal research funding remains as yet unaffected. Does this mean that grant-funded APC-based revenues may serve as some kind of safe harbor? Is the pivot that some companies have made towards tapping budgets from the research enterprise, especially for workflow and analytics tools, another area of comparative growth? And, in the drastic pivot to online learning this spring, certain instructional tools have value beyond what anyone could have projected. Are there other opportunities to support the undergraduate curriculum directly, such as those by APA described so well by Jasper Simons in his talk during the recent STM US meeting? In an environment of austerity, publishers and other information providers will have to make choices about the markets and channels they should work to engage. There may be strategic opportunities amid the uncertainty.