[Editor’s note: This is an updated version of an essay that first appeared in The Journal of Electronic Publishing. Joe would like to thank Judith Axler Turner for her editorial assistance on the first version.]

Let’s stop talking about sustainability and start talking about growth.

The Context of University Press Publishing

The notion of sustainability has become something of a mantra in the university press world. The narrative goes something like this: Once upon a time, before predatory commercial journal publishers began their assault on the purchasing budgets of academic libraries, libraries could be counted on for a certain level of sale of academic monographs. That virtual guarantee permitted university presses to support the research activities of scholars, especially in the humanities. But when the library budgets began to get gobbled up by the villainous commercial houses, monograph sales plummeted, taking the fortunes of university presses with them. Thus, the goal is to find a new business model, a “sustainable” one, which would enable the presses to continue with their historical support of the research community.

That narrative is largely true.

“Sustainability,” however, is the wrong term to bring to this; at a minimum, let’s elevate it to something more useful: a strategy for economic viability. The problem with the concept of sustainability is that it often confused with “maintainability”; that is, it is rooted in the view that the current situation is something that is indeed worthy of being sustained. This is not true for many presses today, which are seeing the support from their parent institutions dropping and some market channels (and, yes, academic libraries in particular) becoming tougher. Sustainability is about the status quo. For a press to have a financially sound model, it has to think beyond the current market situation and anticipate the shape of the future market. This puts the stress on innovation: What will the future look like, what role do I hope to play in that future picture, and how do I get there from here? The key to a strong business model is not cost-cutting and retrenchment, but identifying new trends and pursuing them.

The five stages of book publishing outlined here comprise a framework to help to look for areas of growth. The five-stage paradigm applies to some degree to all segments of the global book industry, but my emphasis and examples are directed specifically to the American university press world. The plight of university presses is unfortunate, as their role in scholarly communications, especially the certification of faculty in the humanities, is an important one and not something that is likely to be shoved aside because of new developments (which are quite stunning in themselves) in digital media for the entertainment industry: There is a place for whiz-bang technical innovations, but it is difficult, not to mention awful, to imagine a world without the reflective study of Erasmus, Darwin, Burke, and Marx. The five-stage typology is not going to pay today’s bills for any university press; it is not going to get a more generous allocation of funds from any university administration; and it is not going to get people or libraries who have stopped buying press books suddenly to jump up waving a checkbook. What I hope it will do, however, is describe some broad trends that I believe are inevitable, and suggest ways to align scholarly publishing with those trends, the better to reap financial gain from them.

Finding the Point of Intervention

Before I jump into Stage One, though, I want to mention briefly the role of the editorial function. The editorial function—What books should we publish? How and where should we invest our capital?—is at the center of all publishing activity, as it should be. A publishing enterprise, however, whether a not-for-profit academic press or a bottom-line oriented commercial house, has to do a great number of things that are not editorial in nature, including arranging for financing, management of human resources (the inarguable number one success factor), staying on top of technology, identifying new developments in the marketplace, etc.

Let’s think for a moment about some of the questions university presses are dealing with every day and ask ourselves: Are these editorial matters? Should a press support the proprietary software of the Amazon Kindle? Do I want to have my books available on the Apple iPad, and if so, in which of the four different ways (the iBookstore, as an application for the iPad designed for individual books, as an application for an entire storefront of books, or via third-party applications such as those from Amazon and Barnes & Noble)? How do I evaluate a comprehensive XML-based workflow? What is my ONIX strategy? How do I deal with international pricing? What balance should a press strike between making scholarly content widely and freely available and the requirement to generate earned revenue to support the organization and its mission?

The list of items that absorb a press’s time goes on and on, and many of the items are simply distinct from the selection of what books to publish. And here emerges the great irony of publishing today: Although we know a publisher by its editorial choices, the organizational and business context in which those choices are made have become increasingly complex, and that complexity is likely to grow even more in the years ahead. The innovations that are likely to sustain and augment a publisher’s editorial strategy are, for the most part, outside the realm of the editors. Thus, to focus narrowly on editorial decision-making is something of a privileged position, which takes for granted all the other work that is essential for those editorial decisions to be made in the first place.

In some circumstances, however, a press’s editorial strategy is identical to its business strategy. Imagine a business environment with stable operating conditions: the channels of distribution are clear and change only slightly; no new technology is disrupting business activity; funding is more or less steady; enrollments in core areas of publication are not dropping and may even be growing; and the role of scholarly monographs in the certification process is mostly unchallenged. This may sound like a highly romantic view of a publishing environment, but in fact it was the prevailing situation until the 1980s. (Different people will suggest different dates as to when university press publishing began to destabilize.) In such an environment, presses differentiate themselves from one another in the only way they can, the only variable, as it were: the publication of superior books. Thus, editorial decision-making does indeed become the heart of a press’s business strategy because all other aspects of publishing are more or less the same for all the competition.

This is not the world we now operate in, of course. There is almost nothing about scholarly publishing that is not changing. Thus, the editorial strategy is but one of many factors that go into a particular press’s success. And this is the reason that university presses today have to think and plan beyond their editorial departments. Ironically, it could be said that the editorial function is just about the only aspect of academic publishing that is not broken today. The books issued from the press world are outstanding, the editors superb. About the only thing one could wish for is that there were even more books—and that there was a way to finance their creation and dissemination.

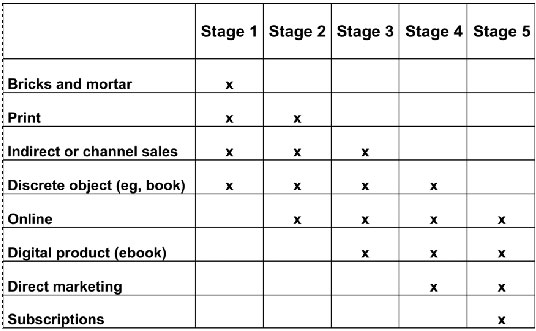

A successful strategy today for a university press is going to have to address the many changes—the ongoing changes—in the environment, and that means engaging the very challenging questions of marketing scholarly books. It’s time to work toward becoming a Stage Five book publisher. To describe what Stage Five will look like, we will track four variables: venue (where a book is sold, whether online or off), medium (whether a book is published in print or electronically), indirect vs. direct marketing (whether a book is sold through intermediaries or directly to the end-user by the publisher), and the sale of books on a stand-alone or discrete basis vs. selling books as part of a subscription.

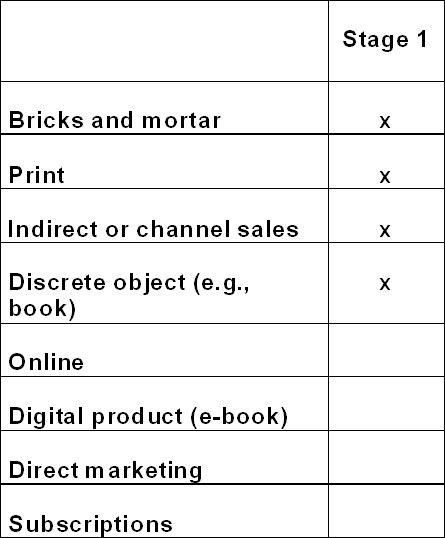

Stage One Book Publishing

Let’s begin by thinking about how we conducted the scholarly book business 20 years ago; we can call those practices Stage One. Twenty years ago, there was no Amazon, iPad, or Google Editions—there wasn’t even a Google—and mobile phones were a rarity. At that time, we all worked in print. We acquired books, after extensive editorial review, and then sent them into the marketplace as discrete objects. For the most part, we sent books to various intermediaries—for example, bookstores and the wholesalers that service libraries. The medium was print; the distribution indirect (that is, through resellers of various kinds); and the entire business was conducted in the world of bricks and mortar.

Virtually everyone working in scholarly publishing knows the Stage One world very well—and with good reason, because most university press publishing is still in Stage One. This is not a criticism of university presses; almost all book publishers of every kind have most of their revenue coming from the Stage One paradigm. But we all know that the elements of that paradigm are changing and usually not for the better. Libraries, for example, buy fewer books today than they used to, and bookstores are having a hard time competing with online venues. So, Stage One is not growing anymore and is probably shrinking, but it is still the largest component of the university press world today. To quantify this, I would say that Stage One comprises 60 to 75 percent of the business of most presses today.

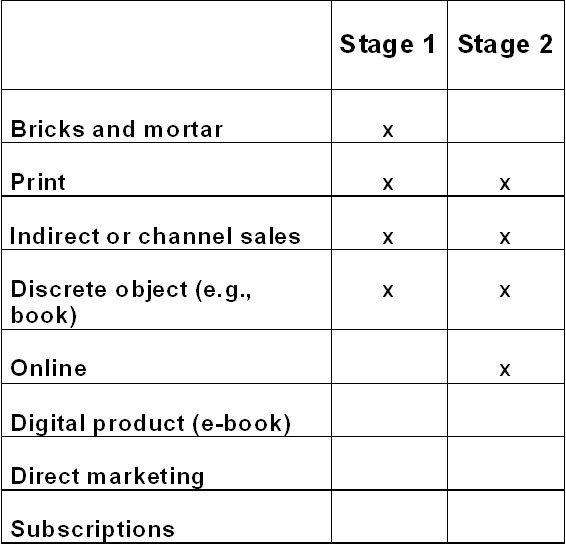

Stage Two Book Publishing

About 15 years ago, Stage Two got started. This is the paradigm for online bookselling of print books, for which Amazon is the exemplar. Over the past 15 years, online bookselling has gone from 0 to 40 percent or more of university press revenue. Even more remarkable is the fact that this growth in online bookselling took place while overall sales were basically flat. As dramatic as this change has been, however, Stage Two still closely resembles Stage One in at least two important aspects: The products are print, and the sales are indirect. Most publishers work with Amazon in the very same way that they work with Barnes & Noble and college stores. Books are printed and placed in a warehouse. When orders come in, the books are shipped to another distribution facility. Rarely does the publisher work directly with the ultimate customer. And despite the fact that the orders are all placed online, using some of the world’s most sophisticated information technology, the product itself is made of dead trees slathered with ink.

.

For almost every publisher, Stages One and Two coexist; together they make up 60-90 percent of total revenue. Most people expect that Stage Two will continue to grow and that Stage One will continue to decline, but it’s self-evident that if you are a publisher, you have to operate in both stages at the same time.

The real theme is inevitability, however, and Stage Two book publishing was inevitable the moment in the fall of 1993 when the Mosaic browser was made available at the University of Illinois. Once the web came into existence, people were going to study it for commercial opportunities; e-commerce was just a matter of time. I was at Encyclopaedia Britannica at the time, and by 1994, we were selling online subscriptions and were considering creating an online bookstore based on the Britannica bibliographies. Amazon was still a couple years off. I have been told, but have not been able to confirm, that Amazon was not the first but the thirtieth bookstore on the web. Amazon, in other words, was not a black swan, a statistically improbable event, but an inevitable development of the web.

The move from Stage One to Stage Two has some interesting implications that all scholarly publishers have had to deal with. Bricks-and-mortar stores are anchored in a particular locale, but online bookselling is inherently global. This disrupts the traditional way book publishers have divided up marketing rights: It is no longer convenient to have one publisher handle sales in the U.K., another handle American sales, etc. The inherently global nature of the Internet thus puts pressure on various copyright agreements. An online bookstore, even one that sells only print books, is thus more than a bookstore. It is also an agent of disruption.

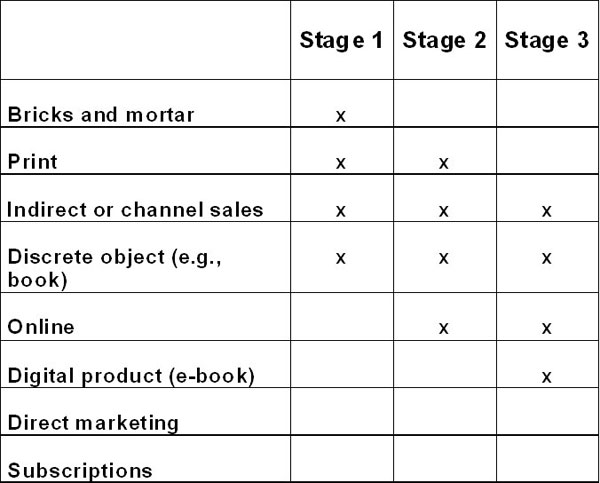

Stage Three Book Publishing

We are now well into Stage Three—which was inevitable—and Stage Three promises to be a doozie. In Stage Three, we continue to have books sold online, but now the medium has changed: The books are e-books. This is a pretty big leap, and it comes with enormous challenges. When we went from Stage One to Stage Two, we didn’t really have to muck around with production or the supply chain very much. You could become a Stage Two publisher simply by shipping more books to Ingram, and Ingram and Amazon did the rest. But when you get to Stage Three, well, how do you get your files into the proper format? And what is the proper format in the first place?

We should pause and think of some of the unprecedented aspects of Stage Three. In just the first month after Apple launched the iPad, Apple became one of the top 10 booksellers in the country; for some publishers, Apple is now number 3. Kindle sales have strengthened Amazon’s already strong position; for a number of publishers, total sales, both print and digital, with Amazon are now over 50 percent of total revenue. While other players have taken a piece of the ebook market, Amazon’s market position is extraordinary and secure.

Stage Three was inevitable; in fact, many people have wondered why it took so long for e-books to take off. In my view, the necessary ingredient was always ubiquitous, inexpensive broadband, as high bandwidth moves the information industry from atoms sold in the physical world to the realm of downloads. There is no known role for bricks-and-mortar bookstores for e-books; once downloads are easy, bookselling accelerates its shift to online services. Stage Three also solves some of the most stubborn problems of traditional bookselling. There is no physical inventory, so there is little cash tied up in inventory. There are no shipping costs. And there are no returns. With those kinds of incentives, the pressure to publish in electronic form was very great.

Most publishers are now well into Stage Three book publishing. Meanwhile, Stages One and Two are still active, so every publisher is now required to run what are essentially three different businesses. The mistake would be to think that these businesses have more in common with each other than they do.

In Stage Three, we have an acute marketing problem: Since people can’t browse in bookstores for e-books, there is a new marketing challenge, and that requires every press to begin to market online. This requires new skills and often different staff. Most university presses are now experimenting with Google AdWords, Facebook, Twitter, and heaven knows what other online service to help people discover books. A couple years ago, I posted a message to a mailgroup about something called search engine optimization. Some people asked me what it was. Now SEO, as it is known, is the single most important marketing tool available to any publisher. This is one of the inevitable aspects of Stage Three, the increasing focus on search engines and Google in particular.

In fact, the focus on search engines began with Stage Two, as publishers began to consider how readers would find their books online. To meet this challenge, many publishers began to put greater effort into the creation of metadata, as it is only through metadata (information about a book) that books have any online presence at all. By the time Stage Three becomes a component of a publisher’s marketing strategy, the management and dissemination of high-quality metadata becomes increasingly important, as a book that cannot be found through an online search cannot be found. It comes as no surprise that the company that has made the biggest investment in metadata of all kinds is Amazon, which almost always is at the very top of Google’s search results for any book. In time (by the time we get to Stage Four), metadata begins to take on new and even more important roles.

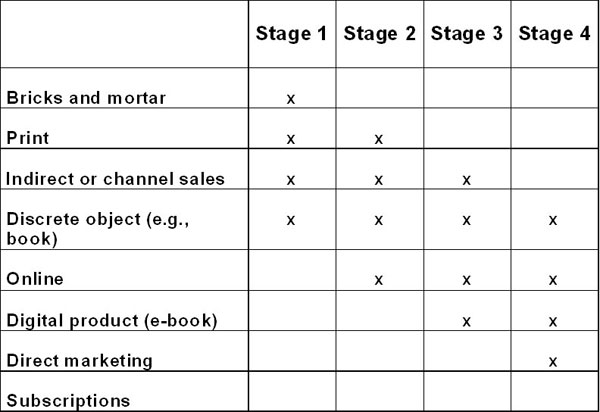

Stage Four Book Publishing

I am insisting on the inevitability of each stage because I want to make the point that the inevitable signs of Stage Four are already emerging. Stages Two and Three began to heighten the need for web marketing and getting a good PageRank in Google. Once a marketer begins to understand how Google works—what I call operating in “the Google ecosystem”—it is just a matter of time before it becomes apparent that it is possible to sell books directly from a publisher’s own website. This is because Google is a portal-buster. Search engine results point to the best presentation of information on the Internet, and for books, often the best source of information is the publisher. You see this every day when you do a search for a news item. Instead of being brought to the home page of the New York Times, you are brought to a page deep within the Times’s site, where the relevant article appears. As publishers work on their own websites, they see the web traffic grow and they are often surprised to see how many people click on the “buy” button. A comprehensive description of a book is the equivalent of a well-crafted story in the Times.

Direct marketing is inevitable—and it is disruptive. In Stages One to Three, we had middlemen, but with Stage Four, we have disintermediated the middleman because search engines make it possible to do so. (The reason we do this is because of the promise of higher margins.) By the time we get to Stage Four, most of the elements of Stage One, bricks-and-mortar bookselling, have disappeared. Print has given way to electronics, physical stores have been replaced by online venues, and channel sales have been replaced by direct marketing.

Some university presses are already experimenting with Stage Four bookselling, and many have been surprised by the result. Typically, people challenge Stage Four by saying, Why won’t people simply go to Amazon? The answer lies in the evidence: In fact, many people do not go to Amazon, even when the price is lower there. There may be several reasons for this: loyalty to publishers’ brands, especially in the not-for-profit sector; laziness (sometimes even one more click is one too many); and perhaps exceptional merchandising online by the publisher.

Does this mean that a press could enter Stage Four and walk away from Stage Three? No. The earlier stages are all important to the overall customer base and a press’s revenue stream. But Stage Four is something different; it is a new marketing opportunity. When publishers get to Stage Four, they put themselves in the driver’s seat. They get to control their marketing messages, they get to test different offers, and they establish a direct relationship with the customer.

That direct relationship tips us into some complicated policy areas. Direct marketers, whether university presses or late-night television household appliance vendors, share a common strategy, and that is to collect as much information about customers as possible. This is not the paranoid surveillance of a Big Brother, but the deliberate tactic of marketers who know from experience that the more information they possess about customers, the more things they can sell. But what about privacy? There is something unpleasant about discovering that your personal information (your purchasing history, your method of payment, your zip code—especially your zip code, which is perhaps the most valuable piece of information for a marketer) is stored in a marketing database, where it is mined for the vendor’s economic advantage. As consumers we might say, Privacy first: Don’t collect any information about customers. But as Stage Four book publishers, we might inquire, How many people are in your household, and what is the outstanding balance on your mortgage?

There is no resolution that I am aware of to the tension between privacy advocates (basically all of us in our consumer aspect) and marketers. The press world is going to have to come up with a standard for marketing practices and data retention. Which begs another question: What if commercial publishers are more lax about their privacy policies? Will university presses prove to be uncompetitive as Stage Four book publishing takes hold?

Stage Five Book Publishing

Stage Four sounds so good for publishers that you would think that they would stop there. The inevitable pressures of technology and the marketplace, however, do not permit this. Inexorably, participants in Stage Four will come to see that they have a very big cost in customer acquisition and they will look for ways to drive that cost down. Enter Stage Five.

Direct marketers know that one of the single biggest expenses they have is getting someone to buy from them in the first place. For this reason, direct marketers are always looking for ways to sell additional things to customers that they already have. I want to make an important distinction here between libraries and publishers. Libraries are interested in the life cycle of a publication, which is why they properly put so much emphasis on preservation. Publishers, however, are interested in the life cycle of the customer. The challenge is how to extract sale after sale from the same person. This is true whether you are an academic book publisher or the head of marketing at Apple.

Stage Five is thus the reemergence of the subscription business. This is a radical change. In all the stages up to now, publishers were still selling discrete objects, otherwise known as books. But once they get their direct-marketing engines running, they will try to convert one-time sales into ongoing sales. There are countless ways to do this and new ideas spring up every day. One way is simply to collect customers’ names and mail them when a new book by the same author or in the same field comes out. Another way is to get people to subscribe in advance to an author’s forthcoming works—in effect, recreating the standing-order plan of the library world for the consumer market. But I think that the real developments in subscription-based book services will come about through the creative use of digital technology in ways that we won’t be able to imagine until someone invents them.

Even before people began talking about “a Netflix for books,” a number of things were put in place that will likely lead to subscription services. If you own a Kindle book that needs a correction or an update, for example, Amazon will make the changes silently over the Internet. Some people find this to be disturbing, as it gets into the hard realm of privacy policy. But it also suggests that Amazon is exploring a subscription model for books. Instead of purchasing (or renting) a book from Amazon, you will subscribe to it, and for that subscription, you get a number of enhancements. It is but a short leap for Amazon to begin to charge for those updates.

In the music world we have a number of growing subscription services: Apple Radio, Spotify, Pandora, etc. Now, what is in Pandora’s Box?, you might ask. What’s there is a new paradigm: Instead of selling music atomistically on iTunes one song at a time, people subscribe to entire libraries. The service is supported by advertising (in effect, it is like listening to a personalized radio station), with a fee-based premium service as an option. Meanwhile, Netflix is streaming movies directly to your computer, tablet, or digital television on a subscription basis. I cannot help but remark on the irony that so many pundits say that the book business is going to move in the direction of the music business, with massive piracy and the equivalent of Apple’s iTunes. Meanwhile, the music business is beginning to look more like the journals business.

It seems probable that all scholarly publishers will become web marketers, direct marketers, and managers of a subscription service in the coming years. If you are thinking about sustainability, the time to begin working on these things is now. Look forward, not back; think innovation, not preservation.

It will be apparent to everyone that a subscription model lends itself to aggregations that are organized by topic. Some of the current projects in the university press world are thus harbingers of Stage Five book publishing, though they are mostly aimed at the institutional market, not to individuals. If you have a collection of titles in, say, political science, you can find all the political scientists and try to attract them to your service. One problem with this model, however, is that only a handful of presses have enough titles in any one category to attract enough subscribers. This naturally leads to having multiple presses combine their titles in order to create a large aggregation. The presence of multiple partners makes it harder for any one press to “own” the customer, which is the point of direct marketing in the first place. Thus, the marketing of aggregations is something of a halfhearted strategy toward full Stage Five book publishing.

Another limitation of the marketing of digital aggregations to institutions is that the institutions themselves, as represented by their libraries’ materials budgets, are short for cash. I know of no scenario wherein the market share for materials purchases for libraries is greater in five years than it is for today. Libraries, in other words, are of diminishing importance to the marketing strategies for scholarly publishers. That doesn’t mean that it is not useful to market aggregations to libraries, but it would be a mistake to stop there.

I expect that Stage Five will result in some restructuring of university presses. Most presses have fairly broad lists; it’s not uncommon to find 10 or more categories represented on a single list. In moving to Stage Five, publishers are likely to work in fewer areas—perhaps only a single area—in order to have the depth of selection that makes subscription marketing effective. I wonder when we will see the first list swap, where one press gives another a small list in one area where the latter press is strong in exchange for a list where the first press has great depth. For subscription publishers, it is better to have a great list in economics than two fairly good lists in sociology and European history. Of course, getting the oversight board of a press to approve such a restructuring will not be easy, but the presses that successfully make this transition are those that will be economically viable tomorrow.

Of course, even as you become a Stage Five publisher, you also have to continue to work as a Stage One publisher, a Stage Two publisher, and so forth. This is the fundamental operating problem for the book business today, the need to straddle multiple business models at the same time. But there is a mistake here that must be avoided, and that is to focus so much on the stages where you already have some revenue that you have no capital to invest in future paradigms. My recommendation is that a press begins to reallocate some resources now, even if it hurts. It will hurt more when the future arrives and you did not get there first.

Discussion

12 Thoughts on "Stage Five Book Publishing: A Guide for University Presses"

I applaud Joe for presenting this illuminating analysis of the different aspects of the scholarly publishing business as it has evolved for university presses over the past several decades. I would only add a few details.

Joe doesn’t talk about the rise of digital printing, but it has played a major role in extending the life of Stages One and Two by making it possible for presses to save on inventory costs through using POD and SRDP (printing “just in time” essentially, rather than “just in case”) and cash flow while servicing a new market of “the long tail” made possible by Google. Those developments have been key to extending the viability of the original print-focused business.

I’m a little surprised to hear that presses have been able to compete with Amazon through direct marketing because Amazon still has the advantage, which most presses do not offer routinely, of free shipping.

Stage Five is interesting to contemplate, but one has to wonder how well the model from music and trade publishing will carry over to academic publishing. It is intuitively obvious that music fans, who have favorite artists they follow, and fans of genre authors in romance, science fiction, etc., would be open to the idea of subscribing to get everything their favorites produce, but it is much less obvious that scholars would want everything written by any other scholar with perhaps the limited exception of those who have achieved “public intellectual” status. Nevertheless, it is an idea worth thinking about, and perhaps some creative marketer at a university press will figure out a way to make this model work for an academic publisher too.

One other point that Joe needs to take into account is the bureaucratic setting in which university presses exist. Unlike commercial academic publishers, they may not have the freedom to do everything they like because of university-imposed constraints. E.g., at Penn State when I was director of the press and we wanted to set up an e-commerce site, we were not allowed to use the university’s domain name because the university did not want to support our e-commerce efforts. Privacy rules at universities may also come into play in affecting how, and whether, presses engage in certain business practices.

I really like this, Joe, and I look forward to sharing it with authors and department heads who seem to think publishing is (a) simple and (b) really only involves print because they can post a PDF of the work on their website and hop! the world will be beating a path to their wisdom. If only.

More seriously, can I add a sixth stage? At OECD, we’ve been a Stage 5 publisher for a number of years (and, yes, we’ve had to re-structure en route and we have to maintain Stages 1 through 4) – but I would argue that we’re now in Stage 6: Freemium.

The new process in Stage 6 is all about using the social aspects of the web and enabling readers to embed and share a read-only, full text, HTML5 version of our publications (or chapters) via their own websites and social media channels – for free. This boosts awareness and readership well beyond the confines of subscriber institutions and those who can afford to purchase on their own account. Aside from the benefits of boosting awareness of OECD’s works (at no cost to our marketing budget), we’re banking on a small percentage of this new audience wanting to trade up to the premium versions (downloadable e-books or print) to help keep the show on the road. I see no reason why this Stage wouldn’t also work for UPs.

Toby Green

OECD Publishing

Toby, where do sales to libraries come in for OECD? The model I presented was presuming consumer sales, not institutional sales. My understanding of what OECD does is that it makes content available for free to consumers, but then markets aggregations with additional services to institutions. Or are individuals purchasing your premium package? This is not an argument for one model over another, but for two different models.

Libraries are pretty central to what we do not only for finding audiences but also for earning revenue. Roughly 80% of our revenue comes from libraries subscribing to our content, the other 20% from individuals purchasing premium services (in which we count e-books and print). As you point out, there’s a limit to the library market and while we expect to see modest growth from libraries in the mid-term (especially outside developed country markets) we are gearing up to offer different premium solutions to individuals beyond simply ‘buy the e-book or printed book’. As you say, two different (and complementary) models.

Welcome to the five stages of my career, and many others too I think! This model for academic publishing has also driven developments in professional bodies and society publishers.

Look at the work of IEEE for instance, or the legal publishing world, or Elsevier’s transition to ebook collections, or the British National Formulary now not just the best-selling prescribing guide in the world but also the best-used app for doctors in the UK. This transition in terms of mix and medium and market has been trundling along inexorably for some time.

At Butterworth-Heinemann in the 1990s much work went into the response to the launch of the first Internet Bookshop (and Amazon was definitely not in the first wave but was the first to wrangle metadata to offer true range properly). As a medium-sized STM publisher, with leading lists among certain professions, the first things that the Internet offered were reach and discoverability; a gift for a specialist publisher as we always struggled to get shelf space. Our own website gave us a route to market which we could also use to collect customer details. We grew direct sales to 10% in about three years, and also added a number of “special sales” customers – non-booksellers such as magazines and equipment suppliers who could add books to their mix using our new-found direct supply capabilities. In this market the ebook has still to find its place, but e-learning offerings are beginning to replace workbooks for professional qualifications.

The challenges of additional cost, margin dilution and new competitors make this a bumpy road; but the route is one that expert organisations such as university presses, scientific societies, and innovative specialists such as http://www.goodfellowpublishers.com can travel with some confidence.

Two thoughts:

1) I’m trying to square the advice in the last sentence of the post — commit resources to be the first arrival at Stage 5 — with Kent’s recent post that scale will ultimately triumph in internet publishing. To me, the two thoughts together imply that most presses starting the journey to Stage 5 won’t be at the finish line. That’s something to think about before committing resources, although I suppose the alternative is to hide under the table. Anyway, the journey is already underway, as the rest of this very good post makes clear.

2) “Stage 5″ is the episode of the Sopranos when Johnny Sack dies. He finds out he’s got Stage IV lung cancer…”and there is no Stage 5,” he says ruefully. Hopefully the Stage 5 in Joe’s schema for publishing is entirely different!

I thought Kent’s post was a good one. The issue of scale, however, applies more to journals than to books. Journals are mostly purchased by libraries, where scale matters. Books are mostly purchased by individuals; this is true for academic books, too. This opens up the D2C opportunity I was writing about. Although librarians increasingly fail to distinguish between journals and books, the marketplace, authors, and readers continue to make that distinction.

Reblogged this on Libraries are for Use and commented:

I can see a model of Stage 5 publishing (essentially ebooks with subscription packages for consumers) fitting in libraries for providing the books needed to fill short-term needs, with purchases of key titles that provide perpetual access via the library’s own (or a consortial) server. This continues a market for UP works while enabling libraries to continue their role in preservation.